ogrtoni0142030

ogrtoni0142030

Revolutionizing Personal Loans for Bad Credit: New Options For Monetary Freedom

In at this time’s monetary panorama, securing a personal loan with dangerous credit can really feel like an uphill battle. Conventional lending institutions usually shy away from borrowers with poor credit score histories, leaving many individuals feeling trapped and without choices. However, current developments in the lending trade have begun to shift this narrative, creating new alternatives for those searching for personal loans despite their credit challenges. This text explores these progressive options, highlighting how they can empower people to regain monetary stability and obtain their goals.

Understanding the Dangerous Credit Panorama

Bad credit score can come up from numerous circumstances, together with missed funds, excessive credit score utilization, or even identification theft. For many, this unfavourable credit history can lead to larger curiosity rates, loan denials, or exorbitant charges. Historically, borrowers with dangerous credit score have been typically relegated to predatory lenders who offered loans with exorbitant interest charges and unfavorable phrases, additional entrenching them in a cycle of debt.

Nonetheless, the panorama is changing. Lenders are beginning to recognize that credit score scores don’t outline a person’s character or their skill to repay a loan. This shift in perspective has led to the development of more inclusive lending practices that consider a broader vary of things past credit scores.

Progressive Lending Solutions

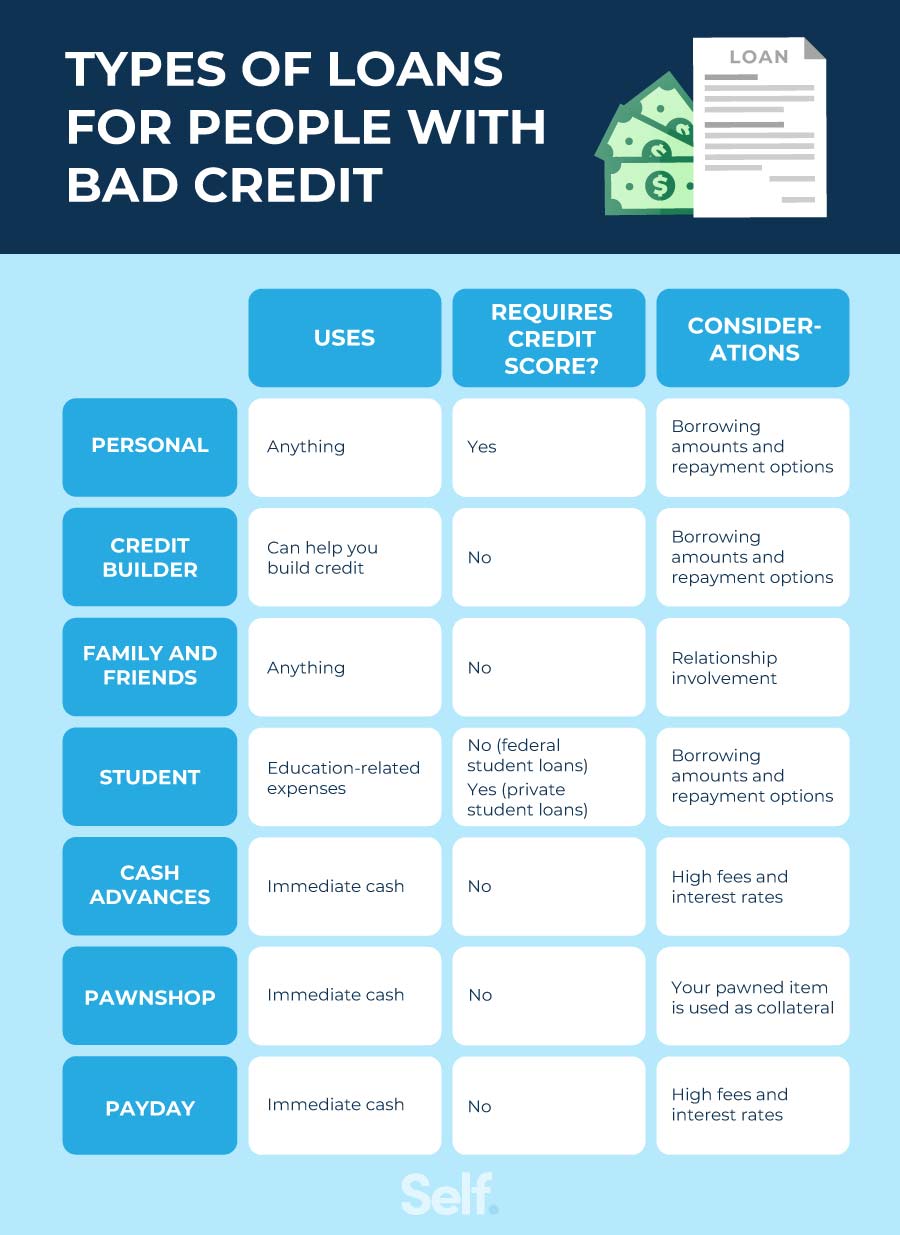

- Different Credit Scoring Models: One of many most significant advancements in personal lending for people with bad credit score is the adoption of alternative credit score scoring models. Conventional credit score scores primarily rely on cost historical past, credit score utilization, and length of credit score historical past. However, newer fashions consider extra components resembling income, employment stability, schooling, and even utility payment historical past. By leveraging these different information points, lenders can acquire a more comprehensive understanding of a borrower’s financial situation and ability to repay a loan.

- Peer-to-Peer Lending Platforms: The rise of peer-to-peer (P2P) lending platforms has additionally remodeled the personal loan landscape. These platforms join borrowers directly with individual buyers willing to fund their loans. P2P lending usually comes with lower curiosity rates than conventional lenders because it eliminates the middleman. Moreover, many P2P platforms are more keen to think about borrowers with dangerous credit, as traders may be motivated by the potential for higher returns relatively than strict credit criteria.

- Credit Unions and Community Banks: Credit score unions and neighborhood banks have lengthy been known for his or her member-focused method to lending. These institutions often have more versatile lending standards and are more prepared to work with people facing credit score challenges. Many credit score unions provide personal loans particularly designed for members with dangerous credit score, typically with lower curiosity charges and extra favorable repayment terms. Moreover, the group-oriented nature of these institutions means they are sometimes invested within the monetary nicely-being of their members, resulting in extra personalised help and guidance.

- Secured Personal Loans: For those with bad credit score, secured personal loans present one other viable choice. These loans require collateral, equivalent to a car or financial savings account, which might reduce the lender’s risk. As a result, borrowers could possibly secure a loan with more favorable terms, even with a poor credit score historical past. Whereas the chance of dropping the collateral exists, secured loans could be a pathway to rebuilding credit score while accessing mandatory funds.

- Fintech Innovations: The fintech business has revolutionized the lending space, introducing know-how-driven options that streamline the loan software process. Many fintech firms utilize advanced algorithms and machine learning to evaluate creditworthiness, allowing for quicker approvals and more personalised loan choices. Additionally, these platforms typically present borrowers with academic assets and instruments to help them enhance their credit score over time.

- Debt Consolidation Loans: For people struggling with a number of high-curiosity debts, debt consolidation loans can be a lifeline. These loans enable borrowers to combine their existing debts into a single loan with a decrease curiosity fee. If you have any sort of inquiries concerning where and how to utilize Personalloans-Badcredit.Com, you can call us at our own internet site. While traditional lenders could hesitate to supply consolidation loans to these with unhealthy credit score, many different lenders and fintech firms have emerged to fill this hole. By consolidating debt, borrowers can simplify their payments and potentially save cash on curiosity, making it simpler to handle their financial obligations.

The Significance of Financial Schooling

Whereas the advancements in personal loans for individuals with bad credit are promising, it is crucial for borrowers to equip themselves with financial training. Understanding credit score scores, curiosity charges, and loan phrases is crucial for making informed choices. Many lenders now offer educational assets, workshops, and online tools to assist borrowers improve their financial literacy. By taking benefit of those sources, people can higher navigate the lending landscape and make choices that align with their lengthy-term financial objectives.

Constructing a greater Financial Future

For individuals with bad credit score, the road to financial restoration may seem daunting, however the current advancements in personal loan choices present hope and opportunity. By exploring various lending solutions, borrowers can entry the funds they want to handle pressing monetary wants while taking steps towards rebuilding their credit score.

/cloudfront-us-east-1.images.arcpublishing.com/dmn/VQTVMZKYXBBLVECIAWNZC46WME.jpg)

It is essential for borrowers to strategy personal loans with caution. Understanding the terms, charges, and interest rates related to any loan is crucial to avoid falling right into a cycle of debt. Moreover, individuals ought to consider making a budget and creating a plan to enhance their credit over time. This proactive approach can empower borrowers to make knowledgeable decisions and work towards a brighter monetary future.

Conclusion

The panorama of personal loans for people with unhealthy credit is evolving, pushed by innovative lending options and a growing recognition of the need for inclusivity within the monetary sector. By leveraging different credit scoring models, exploring peer-to-peer lending, and searching for help from credit unions and fintech corporations, borrowers can find pathways to financial freedom. As the lending industry continues to adapt, individuals with unhealthy credit can take coronary heart in realizing that there are choices out there to help them overcome their monetary challenges and construct a more secure future.